This article is an excerpt from the InvestorPlace Digest newsletter. To get news like this delivered straight to your inbox, click here.

Nvidia’s (NASDAQ:NVDA) second-quarter results on Aug. 23 should have been a triumph for AI enthusiasts. The Silicon Valley chipmaker beat revenue estimates by 20.3% and net profits by 29.5%. These stunning figures would ordinarily send any stock soaring. Or at least give bulls some hope for future earnings growth.

But investors would have been disappointed on both counts. Nvidia’s stock rose less than 1% over the following week — a tiny fraction of what bulls might have expected. And instead of future developments, Nvidia’s management announced a $25 billion stock buyback program. These programs are typically designed to shrink companies and boost earnings per share once growth begins to slow. Apple (NASDAQ:AAPL), for instance, started its share buyback program in 2013 just as iPhone profits reached a downward inflection point.

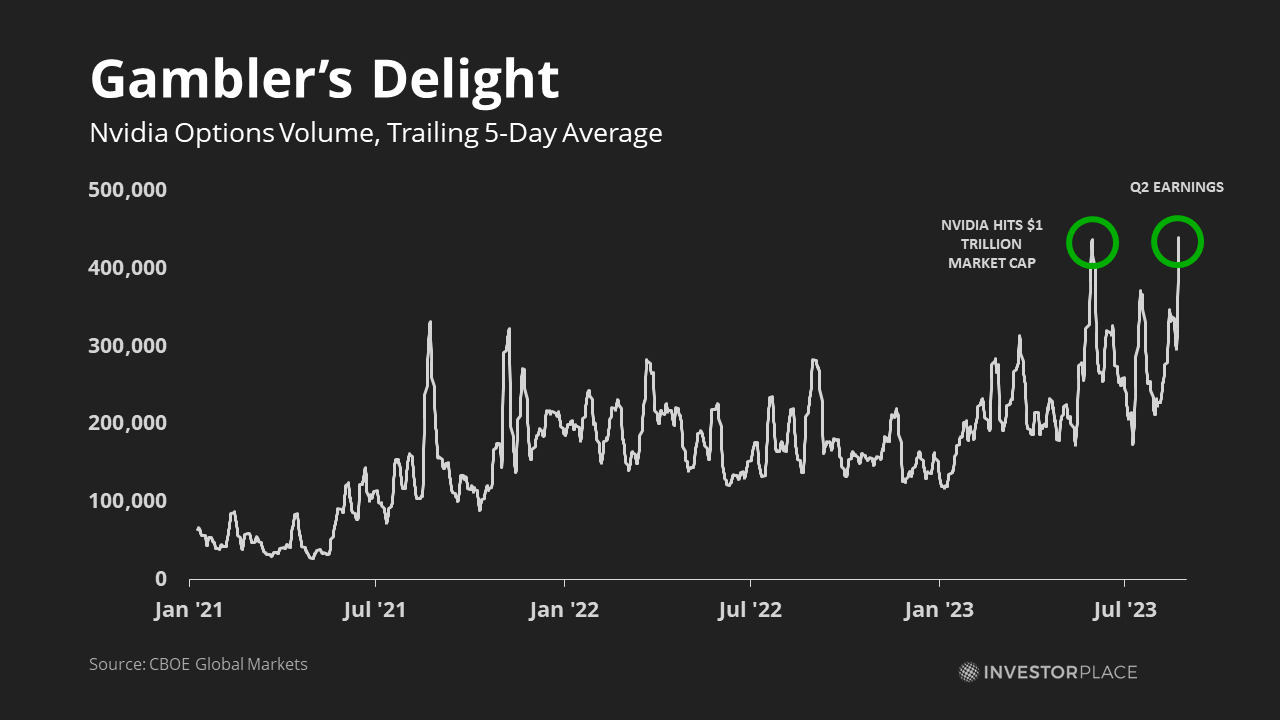

Instead, the real winners of Nvidia’s boom have been options traders… or at least its market makers. These speculators often care little about what an underlying company does. As long as the underlying asset promises to move in a predictable direction, these gamblers are more than happy to buy in. Activity in Nvidia’s options has risen eightfold since 2021, and InvestorPlace.com contributor Michael Gayed has gone as far as to call Nvidia a “source of liquidity” — a term usually reserved for either the Federal Reserve or “The Bank of Mom and Dad.”

This isn’t the first time a new technology has become a zero-sum betting game. In 2017, Bitcoin (BTC-USD) became a de facto casino after its futures were listed on the highly liquid Chicago Mercantile Exchange. Over $50 trillion in Bitcoin has since changed hands despite the crypto’s inability to find many real-world uses. Japanese real estate in the 1990s and Chinese tech stocks of the 2000s share many similarities. At the height of the 2008 and 2014 Chinese stock market bubbles, many day traders admitted to only knowing their investments by their six-digit tickers. As the mystique of artificial intelligence grows, Nvidia’s shares risk falling into the same trap.

Castles in the Sky

First, it’s important to note that Nvidia has some significant differences from cryptocurrencies. The former is a business that generates cash flow; analysts expect Nvidia to generate up to $30 billion in free cash flow this year. The chipmaker is also a picks-and-shovels play on artificial intelligence, a field with fewer established alternatives to crypto payments. Meanwhile, Bitcoin and other cryptos typically generate no internal cash flows. (Cash generated from staking is more like money-lending). Real-world adoption of these coins also remains limited to a handful of companies and super-fans.

But Nvidia and Bitcoin also share a lot in common.

Consider valuation. Today, Nvidia’s $1.13 trillion valuation represents a 240X multiple of trailing earnings, making it the most expensive tech stock based on normalized figures. Even if the chipmaker raises its net income 8X from $4.37 billion to $37.96 billion by fiscal 2026, the company would have to keep increasing that figure by 7.3% per year for the next two decades to justify its current share price of $470.

As for its lofty $622 Wall Street price target? Nvidia will have to generate $145 billion of free cash flow by 2042 to justify that valuation, 2.5X more than what Microsoft (NASDAQ:MSFT) makes today.

There’s also growing evidence that traders are piling into NVDA stock to gamble. According to Fintel, net gamma exposure to Nvidia’s stock reached as high as $636.61 earlier this week after speculators bought an enormous number of bullish call options. For every 1% Nvidia’s stock price rises, market makers will now lose roughly $636.61 million, compared to $0 in 2022. The entire market capitalization of Nvidia now also turns over once every 30 days, compared to 65-80 days in previous years.

That makes Nvidia more like Bitcoin than a promising semiconductor stock. As Josh Enomoto notes on our free news site, InvestorPlace.com, target prices are getting driven ever higher by credulous Wall Street analysts.

Management Knows Nvidia Isn’t Worth $1.13 Trillion

Nvidia’s management clearly understands the disconnect. During the company’s Q2 earnings call, chief financial officer Colette Kress announced that the board approved an additional $25 billion for stock repurchases to add to its remaining $4 billion authorization. The firm also returned roughly $3.4 billion to shareholders during the quarter through share repurchases and dividends. To them, it’s more important to return cash to shareholders at high valuations than it is to hold onto a large war chest.

This tells us that management has little use for the excess cash that the AI gold rush is creating. Nvidia is a fabless chip designer that outsources its production to third-party providers. Unlike Intel (NASDAQ:INTC), Nvidia does not need to spend billions on creating “fab” chip factories. It also sees little potential to acquire future growth, like what Advanced Micro Devices (NASDAQ:AMD) did in its $49 billion acquisition of networking giant Xilinx.

But speculators seem to care little for such truths. To them, Nvidia is an investment in AI. And the only direction it can go is up.

According to data from Refinitiv, open interest for bullish call options has exploded in recent weeks. The number of $500 calls due January 2024 has risen more than 175%, even as Nvidia’s stock has flatlined. These risky bets pay nothing unless the stock rises above $500 by early next year.

Bitcoin saw similarly bullish bets during its 2021 run. Futures contracts for the cryptocurrency traded as high as $65,900 toward the bubble’s peak as investors continued expecting more gains. That story ended as most bubbles do.

What Is Nvidia Stock Worth?

Realistic estimates now peg Nvidia’s justified value at around $350 per share. This assumes that its free cash flow peaks in 2026 at $52.5 billion before declining to $42.5 billion by 2046 as competitors eat away at the lower end of the market. These figures are still well above Intel’s peak earnings power in the 2010s.

There’s also a great deal of potential downside. If companies like Microsoft and Alphabet (NASDAQ:GOOG, NASDAQ:GOOGL) successfully develop in-house GPUs, Nvidia’s free cash flow could recede to the $5 billion to $10 billion range, sending the stock’s justified value into the $200 range. And if free cash flow collapses back to 2020-22 levels, NVDA stock could sink as low as $110.

Of course, none of this matters in the short term. The chipmaker is riding a tidal wave of positive sentiment, which means its stock could rise to $600… $800… $1,000… or more. Nothing stopped Bitcoin from peaking at a $1.27 trillion valuation, or altcoins from rising even further. We know from history that speculative assets tend to keep going up in the short run.

But when the AI hangover eventually comes, we can expect financial historians to ask the age-old question:

“What were they thinking?”

That’s why investors should view Nvidia’s near-$500 price tag with deep suspicion. Companies like Qualcomm (NASDAQ:QCOM) and Intel trade for roughly a tenth of its valuation from a price-to-earnings standpoint. And though Nvidia is winning the AI revolution so far, history also tells us that no castle in the sky has ever stayed aloft forever.

As of this writing, Tom Yeung held a LONG position in GOOG, GOOGL. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.